Canada’s group benefits system has long operated on a simple premise: reimburse care after it happens. But as digital expectations rise and access challenges persist—particularly in mental health—that model is starting to show its age.

French healthtech unicorn Alan is betting that a different approach can take hold in Canada. With the recent launch of Alan Clinic in Ontario, the company is moving beyond traditional insurance to embed care directly within its platform, allowing members to understand their coverage and book therapy in one place.

For Mark Goad, General Manager of Alan Canada, the shift reflects a broader rethink of what insurance should be. Rather than acting as a passive payer, he argues insurers can play a more active role in helping people access care earlier—reducing friction for patients while aligning incentives around prevention and outcomes.

For Mark Goad, General Manager of Alan Canada, the shift reflects a broader rethink of what insurance should be. Rather than acting as a passive payer, he argues insurers can play a more active role in helping people access care earlier—reducing friction for patients while aligning incentives around prevention and outcomes.

In this conversation with Fintech.ca, Goad discusses why Canada’s benefits model has been slow to evolve, what a “full stack” insurance platform looks like in practice, and how integrating care, payments, and digital infrastructure could reshape the future of insurance in Canada.

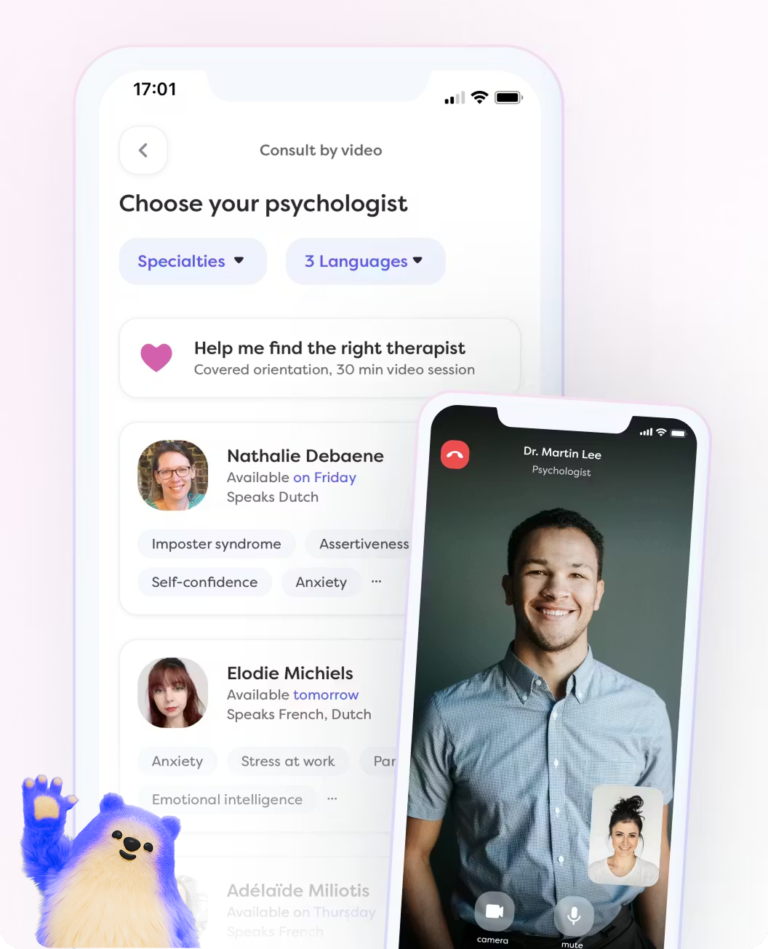

Alan recently launched Alan Clinic in Ontario. What’s fundamentally broken in the Canadian insurance model that led you to build this?

MG: The Canadian benefits model was built around reimbursement.. Insurance typically steps in after care happens. An employee finds a provider, pays upfront, submits a claim, and waits to be paid back. On paper that works. In practice, it creates friction.

In mental health especially, access is the real issue. People may have coverage, but they face long wait times or a confusing path to actually use their benefits.

We built Alan Clinic in Ontario because we think insurance should help people access care, not only reimburse it. By embedding licensed therapy directly inside the insurance platform, members can understand their coverage and book care in the same place.

It sounds simple. But structurally, it’s a different model.

Why do you believe the Canadian model is outdated?

MG: Canada’s group benefits market has historically been dominated by a few large players. This lack of competition has made it slow to evolve. The system works, but it wasn’t built for a digital-first environment. Many core processes are still built on older infrastructure. Claims systems, underwriting models, and vendor networks were not designed for a digital first world.

Employees now compare their benefits experience to the rest of their digital life. Employers are also looking for solutions that are simpler to administer and easier to understand. The legacy reimbursement-heavy model struggles to meet those expectations.

What we’re seeing now is a shift toward embedded services. By integrating care directly into the insurance platform, you move from being a passive player to an active partner in helping people access support earlier. Technology allows you to unify scheduling, eligibility, payment, and clinical coordination in one platform.

It also changes incentives. When insurers only reimburse, the focus is on cost containment. When care is embedded, there’s greater alignment around early intervention and preventing escalation.

You’ve described Alan as “full stack.” What does that actually mean in insurance?

MG: Full stack in insurance means owning the entire experience (from underwriting and coverage design to payments, care access, the member interface), rather than relying on patchwork of third-party providers.

By building these layers ourselves, we can simplify how people access care. Alan Clinic, for example, is our in-house mental health practice. Therapists working with Alan benefit from structured onboarding, ongoing clinical supervision, and a global peer consultation network led by clinical experts.

This digital infrastructure reduces administrative burdens, allowing providers to focus on patient care. Whether a member is booking a teleconsultation or submitting a claim – ultimately, the technology works best when it quietly removes friction for both members and clinicians.

How can digital access address growing concerns like mental health?

MG: Mental health is one of the largest and fastest growing areas of spend in Canadian group benefits. The challenges here are cost, access, and early intervention.

If employees face long waits or unclear processes, they delay care. That often leads to more complex needs later.

Digital access reduces those barriers. When therapy is embedded within the insurance platform, members can see their coverage and book licensed clinicians without navigating separate reimbursement flows.

Earlier access tends to improve engagement and reduce escalation. For employers, it also simplifies the ecosystem by reducing reliance on multiple disconnected vendors.

Privacy is a major concern when healthcare and digital platforms intersect. How does Alan approach data protection?

MG: Trust is fundamental, especially when mental health is involved. Alan Clinic was designed so that clinical care and insurance data are structurally separated.

Therapy sessions are end-to-end encrypted and never recorded. Clinical notes are stored on Canadian servers only accessible to clinicians. Alan, as the insurer, does not have access to session content, and employers never receive identifiable data.

What does this signal about the future of digital insurance in Canada?

MG: We believe Canadian insurance is entering a phase of integration.

Historically, insurers processed claims after care occurred. Going forward, digital platforms make it possible to integrate coverage, payments, data, and care access in one environment.

Technology, including AI, will increasingly automate underwriting decisions, reduce manual claims work, and enable better care routing.

The insurers that modernize their infrastructure will compete on experience and outcomes, not only on price. That shift is already underway in other markets, and Canada is beginning to see it as well.

Leave a Reply